- 09/09/2025

- Posted by: Sandra Borma

- Category: News

Agriculture plays a critical role in Sub-Saharan Africa (SSA)— the sector employs nearly half of the workforce[1] and drives food security, rural development, and poverty reduction. At the heart of this sector are agricultural micro, small, and medium-sized enterprises (agri-MSMEs)—the backbone of SSA’s rural economy. However, despite their importance, agri-MSMEs face a persistent barrier: access to finance.

With three out of four agri-MSMEs unable to secure bank loans[2], these enterprises struggle to grow, innovate, and contribute to the region’s sustainable development.

This article delves deeper into the key challenges behind this financing gap and how COLEAD is working to address them.

The financing gap: a barrier to growth for Agri-MSMEs

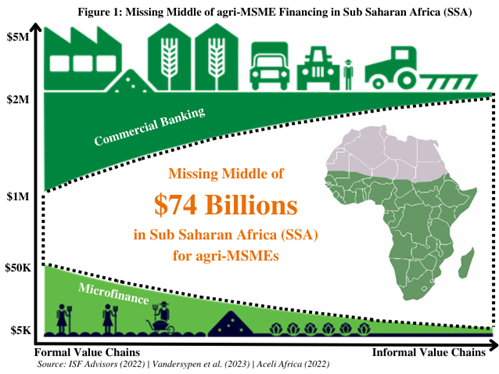

Agri-MSMEs in SSA are caught in a financing paradox: they are often too large for Microfinance Institutions (MFIs) but too small or risky for traditional banks and investors.

This has created a $74 billion annual financing gap, leaving approximately 84% of the demand for funding unmet[3]. The most acute need lies in the “missing middle”: the funding requirements between $50,000 and $1 million[4] (Figure 1). This gap stifles the growth of thousands of promising agri-MSMEs, limiting their ability to scale, create jobs, and contribute to food security and economic development of the region.

Key blocking factors to accessing finance

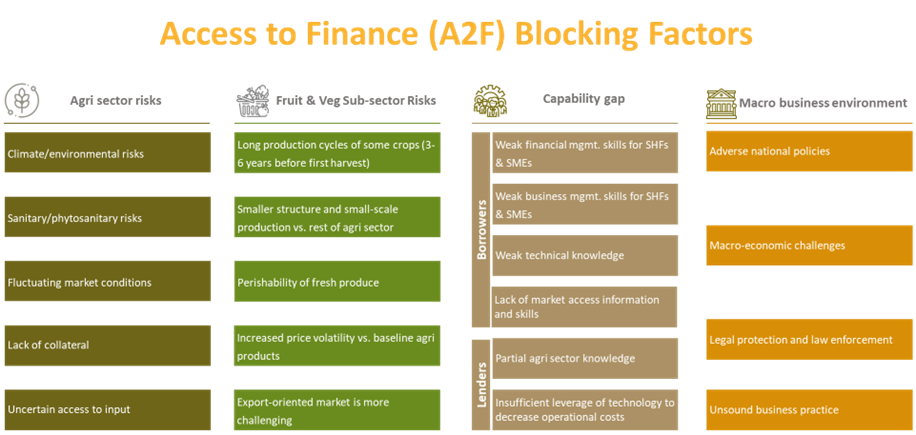

To contribute to solving the access to finance challenge in Sub-Saharan Africa (SSA), COLEAD has identified the key blocking factors agri-MSMEs face, which fall into the following four categories:

- Agri-sector risks:

Agri-MSMEs in SSA operate in a high-risk environment that limits their access to finance. Climate variability, pest outbreaks, and phytosanitary issues can cause significant yield losses, increasing the risk of default. Market volatility, perishability, and weak storage infrastructure further affect their reliability as borrowers. Many also lack formal land rights, collateral, or transaction history, making credit access difficult. Further, uncertainty about the availability and quality of inputs such as seeds, fertilizers, pesticides etc. also impact them directly their income and then in turn their ability to repay.

- Fruit & vegetable sub-sector risks:

The fruit & vegetable value chains (sub-sector of the agri sector) face even higher hurdles. There are usually long production cycles (3-6 years for some crops), small-scale operations, and fragile supply chains, which raise the risk profile. Further, perishability and lack of cold chains lead to post-harvest losses, while entry into export markets is hampered by price instability and high compliance barriers.

- Capability gaps:

The capability gap can be observed both on the borrower and the lender side.

From the borrowers’ side, many agri-MSMEs lack financial management skills (e.g. budgeting and cash flow management), and business management expertise (e.g. marketing, HR, strategic planning, etc.). Limited access to market information also makes it harder for agri-MSMEs to plan or negotiate effectively. On the technical side, poor farming practices often lead to lower yields. It is on this category that COLEAD focuses its efforts, providing capacity building to borrowers to equip them with the right skills and knowledge to be investment-ready.

On the lenders’ side, the lack of agri-specific knowledge hinders their ability to craft lending products that are adapted to the sector. Traditional credit assessment processes also create high operational costs when applied to this sector, while use of technology (e.g. automated scoring, Geographic Information System, etc.) could make it more attractive.

- Macro environment challenges:

Macro challenges also contribute significantly to the financing gap. Inconsistent agricultural and trade policies, weak government support, and unclear land rights make long-term investments risky. On top of that, economic instability like inflation, currency devaluation, and political uncertainty raises input costs and affects market performance. Weak legal systems and poor contract enforcement further discourage lenders. In some cases, MSMEs also engage in informal or unclear business practices, which lowers their credibility with financial institutions. The ripple effect of the financing gap

The lack of access to finance has far-reaching consequences. It limits agri-MSMEs’ ability to invest in productivity-enhancing technologies, expand operations sustainably, and access new markets. This, in turn, hampers rural development, exacerbates food insecurity, and perpetuates poverty. Bridging the financing gap is not just about supporting individual businesses—it’s about unlocking the transformative potential of the entire agricultural sector in SSA.

COLEAD’s role in addressing the challenge

At COLEAD, we recognize that addressing the access to finance challenge requires a holistic approach. Our Access to Finance department is dedicated to empowering agri-MSMEs through scalable training programmes, targeted technical assistance, and strategic partnerships with funding ecosystem players. By equipping agri-entrepreneurs with the tools, knowledge, and connections they need, we aim to bridge the “missing middle” and drive sustainable growth in SSA’s agricultural sector.

Looking ahead

The financing gap in SSA’s agri-sector is a complex issue, but it is not impossible. By addressing the root causes of the challenge and fostering collaboration among stakeholders, we can unlock the potential of agri-MSMEs to drive economic growth, enhance food security, protect the environment and lift millions out of poverty. In the next article, we will delve deeper into COLEAD’s solutions and how we are working to make external funding more accessible for agri-MSMEs in SSA.

This activity is supported by the Fit For Market Plus (FFM+) programme, implemented by COLEAD within the Framework of Development Cooperation between the Organisation of African, Caribbean and Pacific States (OACPS) and the European Union. This publication receives financial support from the European Union and the OACPS. The content of this publication is the sole responsibility of COLEAD and can in no way be taken to reflect the views of the European Union or the OACPS.

Notes

[1] The World Bank Group (2023) – World Bank Open Data Portal. https://data.worldbank.org

[2] USAID (2023) – Bridging the Gap: Financing Africa’s Agricultural Growth

[3] Advisors, I. S. F. (2022) – The state of the agri-SME sector-Bridging the finance gap. Commercial Agriculture for Smallholders and Agribusiness (CASA).

[4] Vandersypen, W., Claes, C., & Serneels, S. (2023) – Impact Investing for the Missing Middle in Agri-Finance. Stanford Social Innovation Review. https://doi.org/10.48558/HDGK-AR18